Why being strategic in raising capital is vital for early-stage founders.

As I was talking to one of my early-stage founders about corporate governance principles, I spotted that what I used to be sharing with him isn't general knowledge. Early-stage founders always here "seek smart capital," but I noticed that founders don't really understand the complete depth of that statement or why it's so important to be strategic when raising capital, especially within the early rounds (pre-seed, seed and Series A).

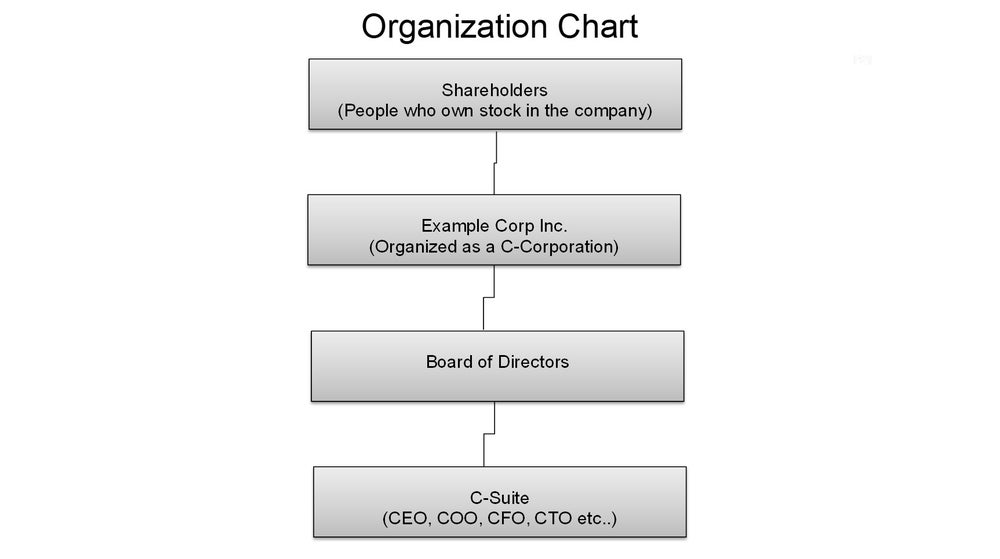

Let's start by changing the phrase "seek smart capital" to "seek synergistic capital." To crystallize the purpose of why seeking synergistic capital is so important for early-stage founders, I would like to hide some key points of corporate structure and governance, as understanding this from that lens will better facilitate your see the importance of the subject. Observe the organizational chart I've created below:

Image Credit: Fredrick D. Scott, FMVA

It's not the prettiest org chart I've ever done, but it'll illustrate now well. The foremost important takeaway from the chart above is knowing how the hierarchy works. ranging from the underside of the chart and dealing our way up:

C-suite executives

C-suite executives are considered "day to day" managers of the business. they're answerable for overseeing and ensuring the corporate and staff are operating within the mission and vision, as outlined by the board of directors (with input from the C-Suite). They make sure the corporation is working, altogether, as efficiently as possible and hitting the varied growth metrics set to make sure the corporation is generating more revenue year after year. Most significantly, you need to understand that a company's C-suite works to the needs and pleasure of the board of directors. This is often a key point of understanding, and you may see why during a bit.

Board of directors

The next level up within the hierarchy is the board of directors. Their job is to supply oversight of the C-suite, to implement macro policy, governance documents and tempo. most significantly, their job is to guard shareholder interests by insuring two things:

One, that the C-suite is working in an efficient manner and steering the corporate within the direction that, within the board's opinion, will cause the simplest possible chance of skyrocketing growth, revenue and profit margins year after year.

And two, that there are proper guardrails in situ that govern the way the C-suite operates and supply sufficient risk mitigants against "irregularities" and/or irrational strategies that, within the board's opinion, would erode shareholder value. More importantly, the board, generally, has the flexibility to effectuate swift action against a C-suite executive within the event that they feel such action would be within the best interests of the corporate, and by extension, the shareholders.

A good example of this played out pretty publicly at WeWork when the now-former CEO, Adam Neumann, was ousted from the very company he founded by the company's board of directors, because (in short) they felt that his actions were now not serving the simplest interest of the corporate, and by extension, the shareholders.

Shareholders

Let's take a deeper study of them. Shareholders (also called stockholders) are the owners of a corporation. They buy stock within the company, and every stock they buy represents a percentage of ownership within the company. How big or small that percentage of ownership depends on what quantity stock the corporate issues and the way many of these stocks an individual or another company (both of which are considered investors) buys. Let's take a look at two very, very simple samples of this:

Company A has issued 100 shares of stock. An investor decides they need to shop for 10 shares of Company A's stock. That investor now owns 10% of Company A.

Company B has issued 1,000 shares of stock. An investor decides they require to shop for 10 shares of Company B's stock. That investor now owns 1% of Company B.

Note that these are, again, very simple examples, and things can get quite a bit more complex than that when gazing at a company's equity structure. However, the aim of those examples is as an instance the purpose that shareholders are part-owners of the corporation.

The importance of seeking synergistic capital

With the above points established, let's examine why seeking synergistic capital as an early-stage company is crucially important. As outlined within the above discussion, it'd seem that everyone seems to be working towards the identical end: to create more cash for the corporation, and successively, make extra money for the shareholders of the corporation. Within the ideal situation, most are aligned completely in this endeavour. However, things are rarely ideal within the world, especially for early-stage companies. While the final word goal is also the identical (to make more money), there will be a divergence of opinions amongst senior executives and therefore the board of directors on the simplest thanks to move towards achieving the final word goal. This divergence is where trouble can begin and where failure can ensue for early-stage companies and/or their founders.

The trouble lies in how the bulk of early-stage companies approach raising capital. Generally, thanks to the very nature of being a startup business and every one the obstacles that come together with that, founders who are attempting to boost capital for his or her businesses (especially within the early rounds), are so desperate for capital that they're willing to require it from anyone who's willing to relinquish it.

The challenge with taking this approach is that, plenty of times, your earliest investors (especially those with experience in early-stage investing) will likely require that they're given a board seat as a condition to providing you with capital. The rationale from an investor's standpoint is that they require to be able to exercise oversight on the corporate — and by extension — the utilization of the capital they furnish the corporate, to confirm that the capital is being employed properly and efficiently.

When a founder understands this fact, what looks as if such a minor thing (giving away a board seat) isn't so minor anymore. Remember, the board's job is to safeguard shareholders' interests and do what they feel goes to drive shareholder value the fastest. Their belief on how it will be done might not align with a founder's vision for the corporation.

Now, lots of founders reading this text will say "Well I own most of my company's shares so this can be a non-issue on behalf of me." which will be true TODAY, however, as you raise more and more capital, you've got to administer away more and more ownership of the corporate (known as dilution), so in short: The more you raise, the less you own. Without proper planning, it's easy to search out yourself, as a founder, within the minority ownership position of the very company you started.

Couple that with a board of directors that does not fully see eye to eye with the way you're running the corporation, and you may easily end up on the skin looking in (meaning fired). Whether or not you're the chairman of the board, it doesn't matter, you'll still be outvoted by the remainder of your board.

Fun fact: Did you recognize that, in step with Roberts Rules of Order (the gold standard for the way to conduct board meetings), the chairman of the board doesn't even get to vote unless it's to interrupt a tie?

This is why seeking synergistic capital is so important for early-stage founders. you wish to make sure that those that are investing in you and your company are fully aligned with you and your vision. you wish people who believe you to assist you add accretive value to your company by way of experience, relationships, and time investment into your development as a founder and CEO (and into the event of the corporate itself). In my opinion, anything in need of this can be a recipe for eventual disaster (remember 94% of venture capital-backed companies eventually fail).

The best chance a founder and their company must succeed is by being strategic and intentional in every aspect of their business endeavours, which is very important within the aspect of raising capital. Founders must remember that working capital doesn't work without companies to take a position in, so it's important to recollect this time, and lift capital as a founder, not as a pauper!

This comment has been removed by the author.

ReplyDelete